Break the Cycle: Clear Debt Without Another Loan

The world is in staggering debt (so is the government). In August 2023, the average household in England owe £2000 on credit cards and £60,000 in overall debt. This is no time to feel guilty or ashamed. Being in debt just helps banks (huge profits for shareholders) and lawyers. Also read posts on giving up lotteries and gambling.

Emma app helps take control of your finances.

If you’re in debt, it’s not going to go away. Get a cup of tea (or large glass of wine), sit at the table and write down how much you owe and to who. Most companies prefer a token payment (it’s less hassle than taking you to court).

Download sample letters (also for business) to offer a payment plan. If no joy, then contact a debt charity (below).

The Multibank has branches nationwide that distribute donated goods to families in debt. You can donate clothes and shoes, unwanted toiletries, bedding and home furnishings, or businesses can donate production-line runs so people can buy or receive goods at the lowest price.

List All Your Debts. Create a detailed list of all your debts. Name the creditors, interest rates, minimum payments, and due dates. A spreadsheet or a simple handwritten sheet works well for this.

Cancel Unused Direct Debits. Many people have thousands exiting their bank accounts each year, due to forgotten direct debits say for insurance or gym memberships. Look through at least the last three months to catch any that might not show up every month.

Calculate Your Monthly Income. Next, you’ll want to determine your net monthly income. This includes salaries, side gigs, rental income- everything. Subtract taxes, savings, and any automatic deductions. What’s left is your spending money. From this, you’ll allocate funds for debt repayment.

Create a Realistic Budget. Separate expenses into fixed and variable. Fixed expenses include rent, mortgage, insurance, and car payments. Variable expenses are groceries, dining out, and entertainment.

Set short-term goals like paying off small debts or saving £100 a month. Long-term goals could be paying off a loan in five years.

Choose a Debt Repayment Method. The Debt Snowball Method pays off smallest debts first, so you are motivated to see them disappear. Once the small debt is gone, roll that payment over to paying off the next smallest debt.

The Debt Avalanche Method focuses on debts with highest interest rates. This method saves you most money in interest payments. This tackles debts that cost more over time.

Pay off essential debts first (energy, water, council tax), and debts to family/friends. Don’t go near payday loans (most are banned). If you’ve got involved with loan sharks, contact a debt charity (below) for advice.

Bailiffs can only enter homes with permission and take goods to sell (TV, furniture, jewellery, cars). They can’t take pets, nor ‘things’ you need (washing machines, beds, cookers, vehicles with disabled badges and ‘home’ camper vans).

Fair for You can help.

Still in Trouble? Contact a Debt Charity

StepChange Debt Charity is funded by industry to provide free help to anyone struggling with debt. Its trained advisors can give advice by phone and there is tons of free advice online. All help is impartial and confidential.

This charity helps hundreds of thousands of people each year. Just tell them your circumstances (don’t worry, they’ve heard it all), and they will then tailor a plan especially for you. Over 30 years, they have managed to help over 7 million people become debt-free, without paying debt consolidation agencies.

StepChange is registered with the Financial Conduct Authority, and does not make money from people it helps. All profits go back into the charity, to help more people.

The range of possible remedies (depending on your circumstances) include:

- Debt Management Plan. This is the main help offered, where your expenditures and income are gathered together, to create a plan that’s affordable yet can clear your debt over time. Your debts are handed over to them, and they create a flat monthly charge to come out of your account, and they take care of the rest. In some circumstances, interest may even be frozen or cancelled.

- Individual Voluntary Arrangements. This is where you pay a reduced rate over a fixed period of time. Once you’ve done this, remaining debt may be written off.

- Debt Relief Orders. This is when debts are written off after a year, if you are on a low income with few assets. There are no fees to pay.

- Debt Arrangement Scheme (Scotland only). This is when you pay back only what you can afford. Trust deeds (also only in Scotland) are where you pay off debts over four years, and again remaining debt is written off.

- Insolvency. If you are considering declaring yourself bankruptcy, contact StepChange that can provide free expert help and advice.

Equity Release. If you are considering releasing part of your home to free up capital, again StepChange can offer free impartial advice, to save you being ‘sold’ anything dodgy. And you can be made fully aware of the advantages and disadvantages/risks, before you make a decision.

Other Trustworthy Debt Charities

- National Debtline runs a good website and phoneline. It has a fact sheet library ((self-employed people can visit Business Debtline).

- Debt Advice Foundation (be careful as others have similar names) is a non-profit with a good reputation.

- Christians Against Poverty (helps people of all faiths and none) can set up a plan to save and pay off debt. Churches can run their free budgeting courses (they also run job clubs to help write CVs and brush up on interview skills).

- Payplan is the non-profit arm of a for-profit company, to help with mortgage problems and negative equity.

Lifestyle Changes to Reduce Debt

- Cancel unwanted subscriptions to gyms, streaming services, magazines etc.

- Cooking at home saves money and is healthier. Plan meals and shop smart to maximise savings. You may even discover a passion for cooking.

- Don’t waste time on energy-comparison sites (listing costs are passed to you). It’s simpler to live simply, this will naturally reduce energy bills.

- Give up smoking and (cut down or give up) drinking alcohol.

- Go car-free or join a car-sharing club.

- Train for a couple of years to do what you love (to earn more money for less hours).

- You could (if viable) downsize to a smaller place (a city flat could be swapped for a small home in a cheaper area). Or rent out a room (tax-free)

- If your family gets on, extended family homes are when relatives sell properties to share one. Say 3 people sell tiny flats to buy one larger garden property (for no mortgage or cheaper payments, with free baby/pet/granny sitting on top).

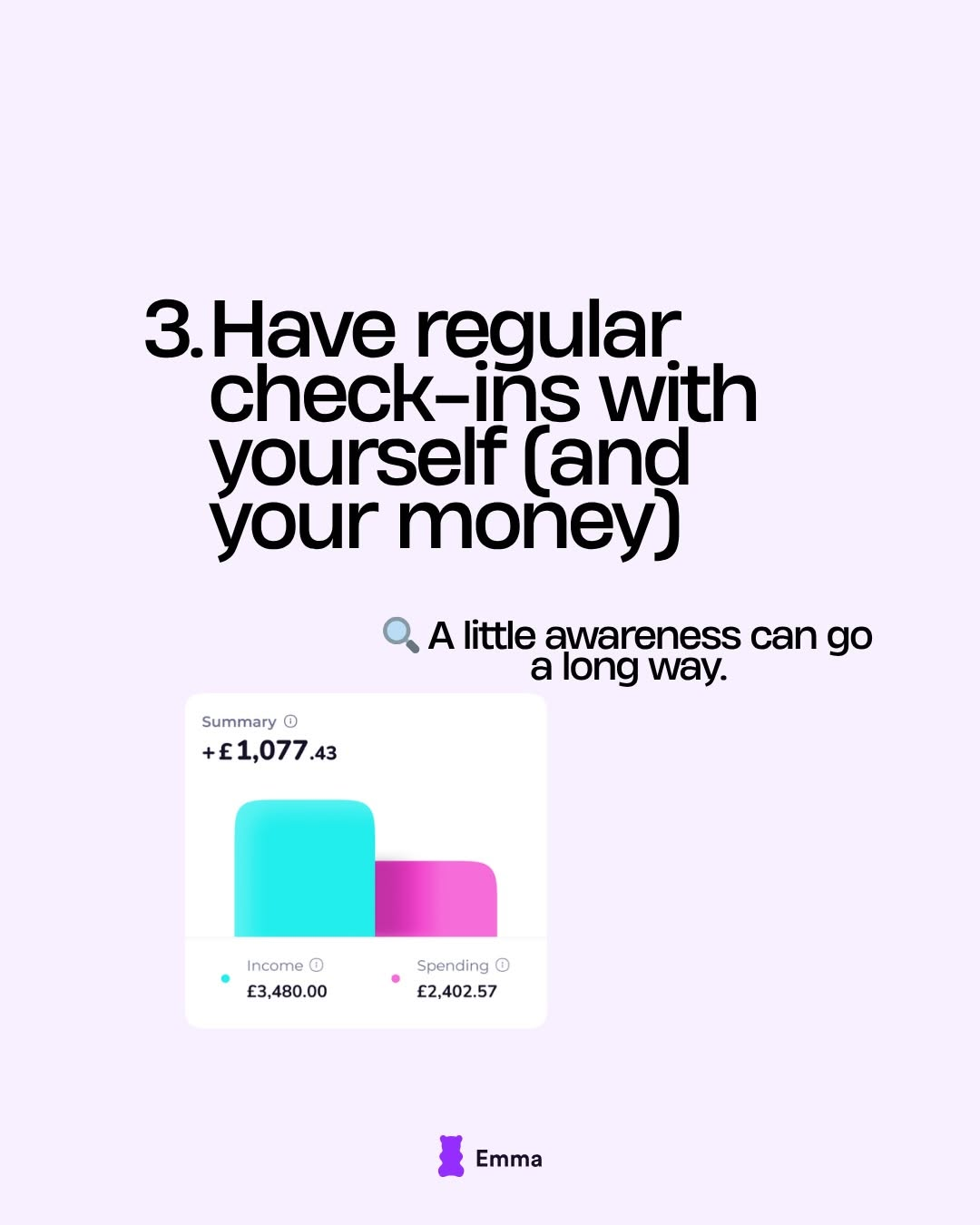

Emma (a simple money management app)

Emma is a simple money management app used by over 3 million people. Just download it (the basic version is free) to spend less and save more.

The powerful tools can analyse your bank account (or accounts) to effortlessly cut spending, and boost your savings, to help keep your goals on track. You can send and request money by sending payment links, or flashing QR codes.

Emma app is safe and secure

Powered by open banking with rigorously tested security, you control data access, and can remoke consent at anytime with no need to share sensitive security details.

Your private is protected by data laws, so only the minimum data necessary is shared through a secure digital process. Emma will never share your information without your consent.

Tech keeps you safe via passwords, PIN, fingerprint or face ID, along with a mobile code or card readers.

Optional upgraded accounts

- Plus lets you set bill reminders so you always know how much money you have left at the end of each month. And get exclusive cashback deals.

- Pro helps you budget like a pro with custom categories and offline accounts. Set smart rules and accurately track your net worth over time.

- Connect connects business account and uses Spaces to manage personal, business and joint accounts.

Budgeting Blueprint: Books to Help Live with Less

Five Steps to Financial Wellbeing is a book to walk you through five simple steps to change your relationship with money, in order to make life better.

Money is not the most important thing on earth, but financial stability lets you live life in line with your values, rather than having to work any job, to stay above water.

It digs into building self-worth without buying things, avoiding debt and investing for the future. The author got out of £27,000 of debt, using the advice she now gives you:

- Overcoming your financial baggage

- Separating net worth from self worth

- Creating money habits and rituals

- Learning to spend mindfully

- Planning and preparing for the future

It’s perfectly possible to live a happy life without abundant wealth. And to live a miserable life with millions in the bank. But it is difficult to live a happy life, if you are locked in a constant battle with your finances.

Get Good with Money is an American book that uses a simple 10-step process created by a former kindergarten teacher who lost her nest egg, when a recession (and encounter with a shady advisor) put her in a huge financial hole.

She used her teaching skills to pay it all off, buy a house and mandate into law financial education for schools in New Jersey. The 10 steps are:

- Build a budget

- Save like a squirrel

- Dig out of debt

- Score high credit

- Learn to earn

- Invest like an insider

- Get good with insurance

- Increase your net worth

- Pick your money team

- Leave a legacy

Stay away from debt at all costs. Debt (not poverty) is the greatest energy of financial well-being and peace of mind. Debt causes us to mortgage our future for the present.

They will dress debt up in a suit, and call it credit. But it all comes down to the same thing. You will have mortgaged your future, to pay for your present. And that is something you never want to do. Kent Nerburn

Where to Find Help for Gambling Addiction

Gambling can seem like harmless fun at first, but for many, it becomes a serious issue that affects every part of life. Whether you’re betting on horses or rolling dice in a casino, gambling addiction can drain your bank account and strain your relationships.

Lying, secrecy, shirking responsibilities are big red flags. Are you finding excuses to cover up a trip to the casino? Neglecting family dinners or missing deadlines at work?

- GambleAware is the main site to help with addiction to gambling, and has a freephone phone number (or live chat) for help.

- It recommends software to block gambling sites like GamBan or GamBlock (the modern equivalent of asking the bookie not to serve you, if your willpower slips).

- The site also has information on self-exclusion (where with one phone call, you can nominate places not to serve you in the surrounding areas (betting shops, online bingo, arcades & casinos).

- Gamblers Anonymous offers help for the addiction often only known by ‘the banker and the bookie’.

Campaigners want a ban to all gambling ads on TV (even if they do add a caveat to ‘be sensible’). It helps also to use free ad-blocking software online.

Coalition Against Gambling Ads wants a complete ban on ads. Of course this won’t happen, as TV companies and the Internet make too much money from them.

So it’s up to us as empowered adults to make the decision to not watch or take any notice of them. Especially when they try to entice with ‘free bets’ to get people to start gambling, who otherwise may never have been tempted.

Any time you offer a big prize for a small amount of money, you encourage stupid behaviour, on behalf of those you’re appealing to. Warren Buffet

Gambling is a tax on ignorance. People often gamble because they think they can win, they’re lucky, they have hunches. That sort of thing. Whereas in fact, they’re going to be remorselessly ground down over time. Edward Thorp

It may help to look up welfare issues for greyhounds and racehorses, rather than just think of gambling in monetary terms.

The Lottery is Another Form of Gambling

Playing the lottery is also a form of gambling (a silly one at that). You’re more likely to get killed by lightning on the way to buying your ticket, than to win it. Quakers refuse lottery funding, saying it takes advantage of desperate people. And order for someone to win, another person has to loses.

Bingo may seem like a bit of harmless fun at the pub, and it probably is. But many people today have spent hundreds of thousands of pounds on online Bingo.

This is not like the old ‘2 fat ladies, 88’ kind of Bingo that your grandma likely played at the community club to win a bottle of plonk. But more big companies advertising on TV, so vulnerable people ending up spending money they don’t have, to try to get themselves out of financially desperate situations.

London’s Notting Hill (not just a big blue door)

The London area of Notting Hill is linked to the Ladbroke gambling family. It is of course known for the blue door, featured in the film of the same name, with Hugh Grant and Julia Roberts. The door still attracts thousands of film buffs each year, in the area known for Portobello Market, which also featured in the stories of Paddington Bear.

The sad truth is that the next door to the ‘door’ is now a Starbucks coffee chop.

There is a little bookshop nearby, but not the one featured in the film, that was filmed elsewhere.

It’s sad that the money in Notting Hill was built from gambling and horse-racing. Today we know better. Much of the land back in the day was owned by the Ladbroke family, and that’s why you’ll find that many roads are named after them. There was even a local racecourse, though that shut down in the 1800s.

Today the area is terribly expensive. You can buy a garage for the price of a normal house. But a quick look online found the cheapest studio flat was around £250K. A luxury six-bedroom house is listed at over £17 million?

Also known for its street carnival, Notting Hill is also known for its colourful buildings, and walkable streets. But as one local says, the clue’s in the name if you’re not that fit – it is of course built on a hill!

Avoid Playing Lotteries (or at least support tiny ones!)

Nearly all lotteries are a scam, as you will hardly ever win (you have more chance of getting killed by lightning on the way to buy your lottery ticket, than you are of winning it!) From scratch cards to complicated odds, the odds of hitting the jackpot is usually 1 in several hundred million.

Lottery Wins Don’t Solve Problems

Lottery wins also don’t solve debt problems? Nearly everyone who wins the lottery loses the money soon after, as it’s more a mindset (receive money, spend it). There is also a suspicion that lotteries are just a lazy way for MPs not to tackle society problems.

For instance, a £4 million jackpot could be divided, for 80 winners each week to pay off the average £50K debt. But then there would be no need for credit cards or mortgages. Food for thought?

Many people of faith refuse to play the lottery. Quakers say that in order to win, someone else (often desperate) has to lose. They refused Lottery funds, as they don’t agree with gambling.

Lottery: a tax on people who are bad at maths. Ambrose Bierce

The universe will throw somebody a bone every now and then, and you win the lottery. But for the most part, you get in this life what you put in. Arian Foster

I despise the lottery. There’s less chance of you becoming a millionaire, than there is of getting hit on the head by a passing asteroid. Brian May (Queen guitarist, badger friend and qualified astrophysicist).

You can still help good causes, just donating to small local charities. You also don’t have to put a big red plastic nose on your face, to help good causes.

The Power of Compound Interest in Savings

Instead, just save the money for a rainy day. You’ll be less stressed and safer too (some people are murdered for their money).

- Save £100 monthly at age 20: By age 60, you could have around £250,000 assuming a 5% interest rate.

- Save £100 monthly at age 30: By age 60, you’d have about £140,000.

To truly appreciate the impact of choosing savings over lotteries, consider these real-life examples of individuals who saved money, instead of playing the lottery:

- Emily: Emily saved £50 every month instead of buying lottery tickets. Over ten years, she built up £6,000. This allowed her to buy a car and take a holiday, enhancing her quality of life.

- James: James spent £5 weekly on lottery tickets for five years. He won small prizes occasionally but ultimately lost more than £1,250 in total. Frustrated, he switched to savings and now contributes to his retirement fund.

- Sophie: Sophie decided to invest her £2 daily lottery money into a savings account instead. In five years, she accrued approximately £4,000, which she used towards her education.

A Caveat (Lottos to Help Animals)

If you do play lotteries, then at least play smaller ones that do real good. Compassion Lottery is run by Compassion in World Farming, which again costs £1 per entry. Match 3 or more numbers to win a cash prize up to £10,000 for six numbers. Winnings automatically go into your bank account, no need to claim.

Veggie Lotto is a small lottery (akin to Bingo or tombola), but still has prizes up to £25K (but cost just £1 a week with 7 guaranteed winners).

50% of all sales go to Vegetarian Society (that is mostly vegan these days) (National Lottery only gives 25% to good causes). One recent recipient was a tiny sheep sanctuary that relies on volunteers.